This is a really interesting question and it’s one people can get wrong and end up wasting precious time with unless they know how to answer it for their own situation. Mostly the answer re whether you should be paying off debt or investing, comes down to the interest or earnings rates in question but there are some important other considerations, and I would like to demonstrate to you, how profound the impact of this decision can be – either in a good, or bad way!! Perhaps you want to create your dream life with supercars and a peacefulness of knowing that everything is taken care of… I hope this article will be a help in you getting there…Let’s jump straight into it…

So should you be paying off debt or investing? It’s all about the rate… – well… mostly!

Let’s say you have a loan worth £10k and the interest rate on this loan is about 6%. If you are considering paying off this loan instead of investing your money in the stock market, my suggestion is that you don’t! There are a couple of caveats which I will go into below, but on the face of it, it would not be wise to clear down the loan. I started my career as a chartered accountant and many thinks make sense to me in terms of what the numbers are saying… so let’s take a look…

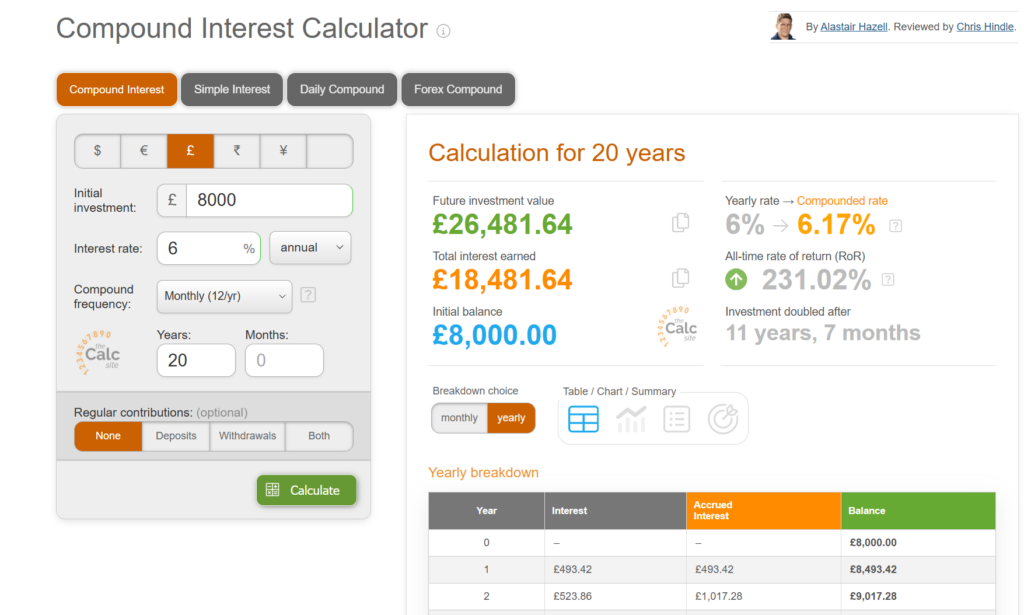

Imagine the scenario where the loan is not getting cleared in terms of capital repayment (so the worst scenario for the loan) and it’s at a rate of 6% interest. Let’s also suppose that this loan will continue to incur interest for the next 20 years. I’ve put these details into the Compound Interest Calculator – here’s a link:

Compound Interest Calculator – Daily, Monthly, Yearly Compounding

I absolutely love playing around with this calculator because it’s like a crystal ball which tells me how rich I will be in the next 10 to 20 years.

OK, so we said a loan of £8k at a rate of 6% with no capital repayments. As you can see above, after a 20 year period, the amount of interest paid relative to the loan appears to be colossal… this is not insignificant in your decision about whether you should be paying off debt or investing, but I wonder whether it will look so big when we compare it to the scenario where instead of clearing down the capital of this loan, the £8k is instead, used to invest in the stock market…

Let’s run the calculator again:

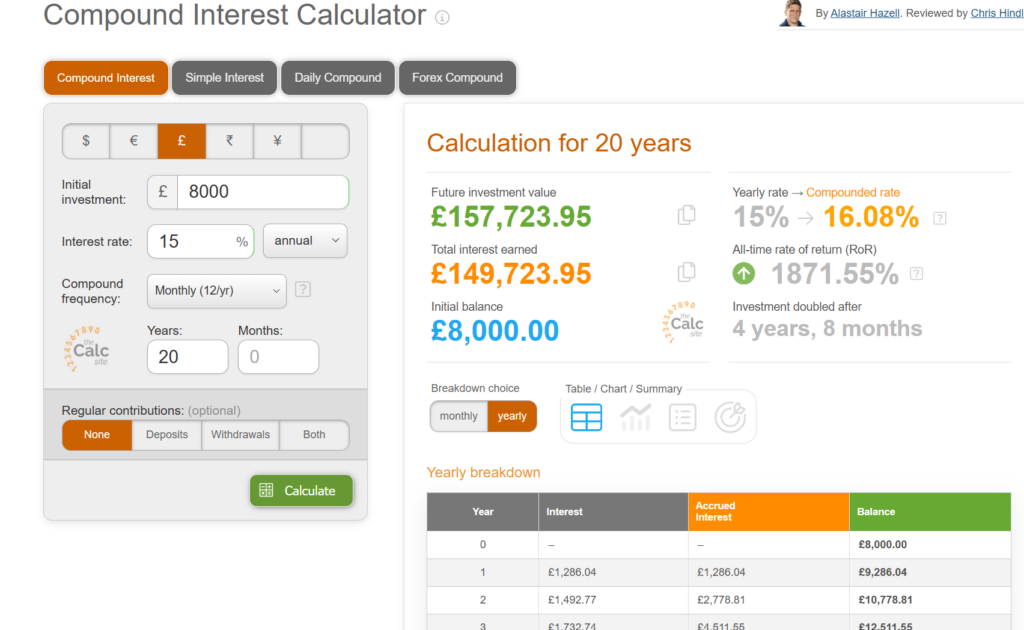

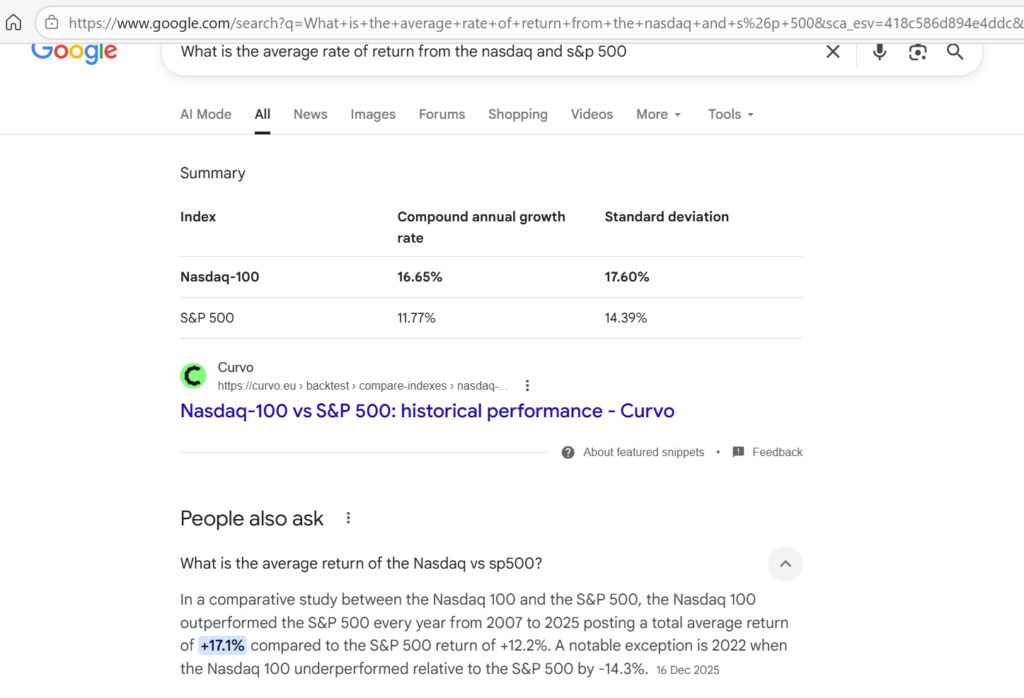

OK, so as you can see I added exactly the same details but just changed the rate. The rate of 15% is not unreasonable in terms of the rate which can be achieved on the stock market, especially when investing in something like the NASDAQ or the S&P 500 – I put the question into Google for you and this is what it answered:

So if you chose instead to invest your money in the stock market as opposed to clearing the loan, you would end up £157,723 – £26,481 = £131,242 better off. You could use some of the investment to clear the loan at that stage but even then!! My suggestion would be to let the investments earn money to ‘slowly pay off’ the loan in instalments! While it’s doing that, the investments are growing still! The answer is infinite when there is a difference in rate, in your favor! I hope this has given you some more clarity on the question of whether you should be paying off debts or investing.

Now, we must acknowledge here, that if you have high interest debts it is better to clear them – because the rate on the debt will be higher.

If you have very low interest debts they lend more weight to the idea of not clearing them and instead, investing the money.

Caveat: I am not a financial adviser – you should consult one before doing anything if you are unsure.

A caveat for you!

OK, so I said there would be a caveat and it’s this: if you are paying off debts, even where they are on a lower rate of interest and you would get a better return on the stock market, it may still be necessary to clear them a bit first – in the scenario where our outgoings are far too high and you are struggling to make ends meet. If finances are a struggle in general and the loan feels like a noose around your neck, it may be good to clear it first. However, just know, once you get to the comfortable stage, if the loan rate of interest is lower than what you can get on the stock market, you would do well to think ‘long term’ and invest the money.

Some inspiration for you- what can you achieve by investing more?

I wanted to share with you some more examples of how much your money could grow over a 10 to 20 year period, especially for someone who is young, but for older people, it’s never too late, and I did write another article on this which is linked below.

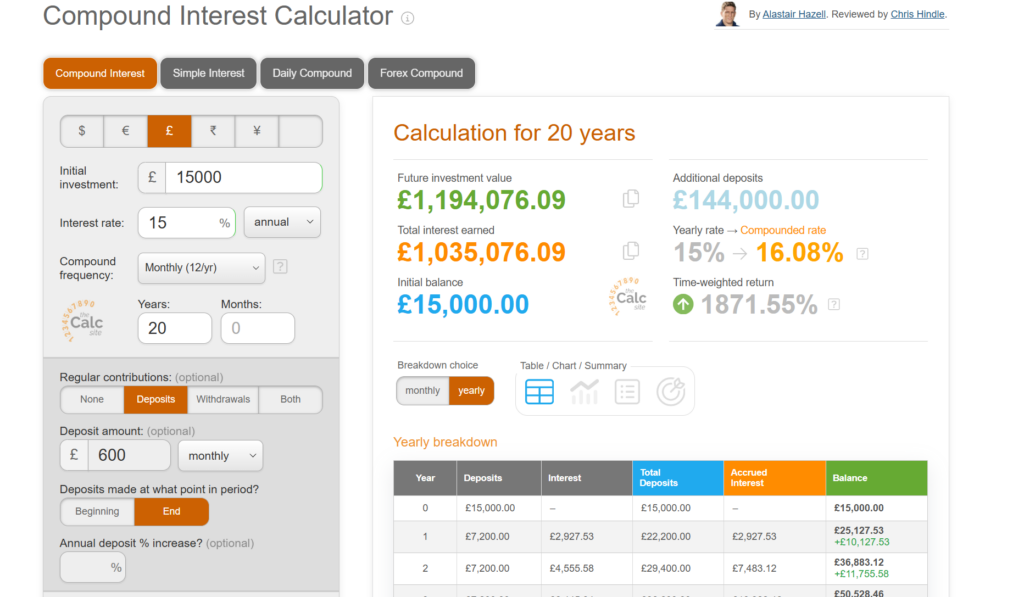

OK, so same calculation again but this time with a higher starting balance and a monthly contribution of £600. This would literally make you a millionaire after 20 years. I know £600 per month is very difficult for some families – especially in the UK but it would still be best to invest as much as you are able. Perhaps you are younger – 18? You could take slightly longer and just put money away more slowly! This is why I like to play around with the calculator.

As promised, here is the video I published about becoming a guaranteed millionaire:

Disclaimer!

Nothing on this blog should be taken as financial advice or encouragement for you to enter a trade. You are expected to speak to a financial adviser or carry out your own due diligence before entering any positions. Everything on this blog is made for educational purposes and to equip you with the knowledge you need to be able to make your own financial decisions.

For more great tips and advice on trading the stock market, please visit:

To watch me trade live please visit my patreon page here:

https://www.patreon.com/Traderpro8320

Finally, if you would like to receive a discount on the Trading View charting software I use, please click on the relevant link here:

https://www.tradingview.com/?aff_id=117138

Please note any subscriptions taken via my affiliate link with Trading View may result in me earning a small commission. However, I provide complete transparency on me using Trading View personally – I publish my success on the financial markets via my broker reports and any profits earned were done so by using my own Trading View subscription, so I genuinely do recommend them and have been using the Trading View charts for many years.